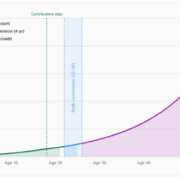

The Retirement Risk No One Plans For

Most disciplined savers don’t run out of money in retirement – they run out of time. The same instincts that built the nest egg can quietly stop you from ever enjoying it. Here’s the retirement risk no one builds a plan around.